Fixing Your Mistakes

Credit scores affect everything from mortgage approvals to job opportunities, yet many people unknowingly undermine their own financial standing. Certain habits can rapidly erode even a solid profile. By recognizing the most damaging behaviors, you can better protect your financial future. So, let's start with 10 actions that tank your credit.

1. Missing Payment Due Dates

Missing a single payment can cause a FICO score to plummet by 90–110 points. Lenders report late payments after 30 days; the damage intensifies the longer a bill goes unpaid. Also, consistently late payments mark you as unreliable to creditors.

2. Maxing Out Your Credit Cards

Carrying balances close to your limits sends a clear signal of financial strain. High utilization—using over 30% of available credit—sharply reduces scores and makes lenders view you as a risky borrower. This can trigger interest rate hikes or account closures.

3. Closing Old Credit Accounts

Shutting down old credit cards shortens your history, which makes up about 15% of the score. It also reduces total available credit. Lenders see a shorter credit history as a warning that you have less experience managing debt responsibly.

4. Applying For Too Much Credit At Once

Every new application generates a hard inquiry, and too many in a short span can dock your score significantly. Clustering multiple applications suggests desperation or financial instability. Lenders often deny applications simply based on a high volume of recent inquiries.

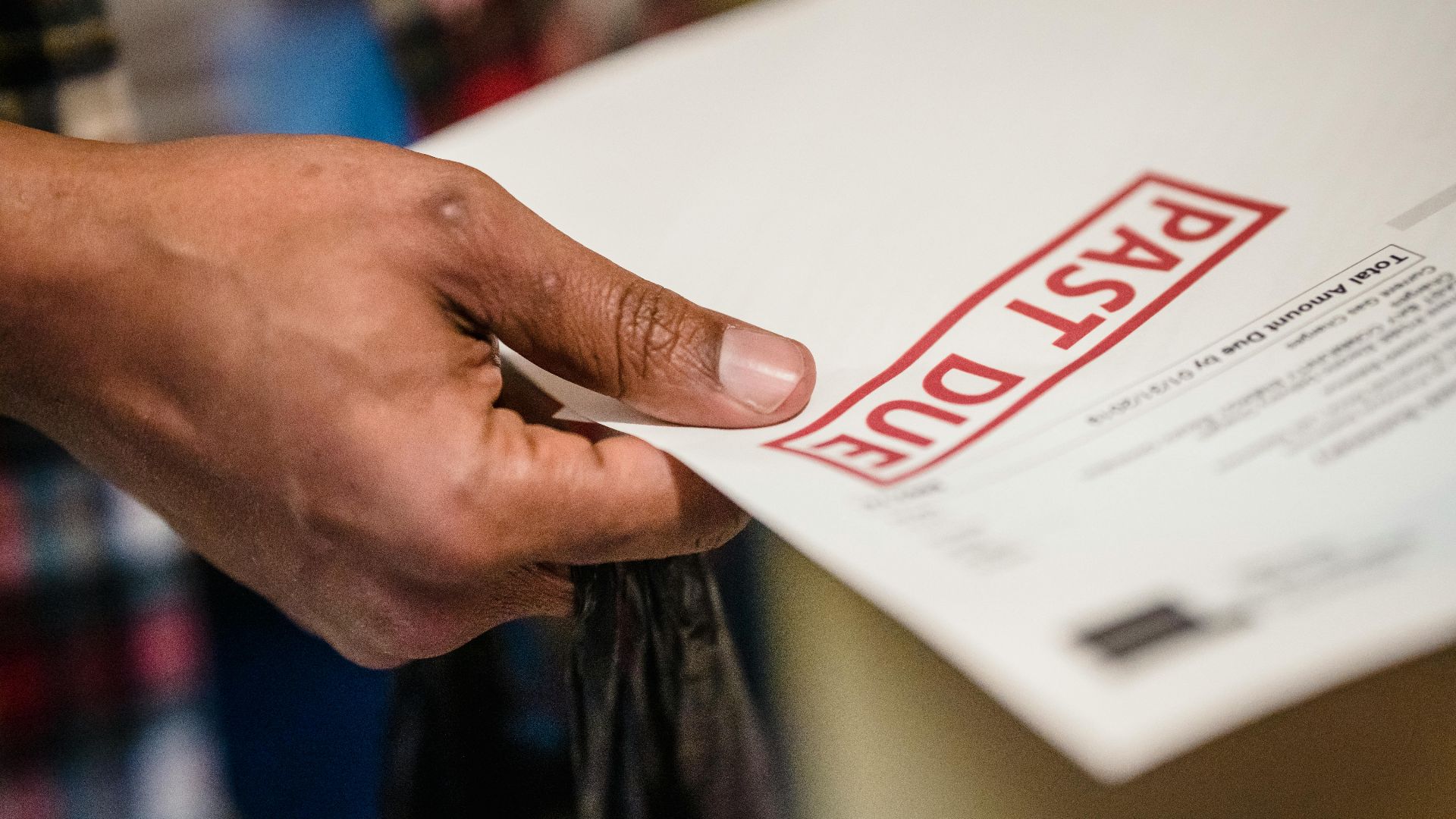

5. Ignoring Small Bills That Go To Collections

Unpaid bills and fines can escalate to collection accounts without much warning. Once reported, they inflict heavy credit score damage and stay on the report for up to seven years. Even minor debts in collections make you appear high-risk to lenders and down goes that score.

Photo By: Kaboompics.com on Pexels

Photo By: Kaboompics.com on Pexels

6. Cosigning Loans Without A Backup Plan

Cosigning exposes your credit to someone else’s financial behavior. If the primary borrower misses payments, the delinquency appears on the report, not just theirs. Lenders treat you equally responsible for the debt; one missed payment can reduce your score.

7. Letting Accounts Go Into Default

Defaults happen after 90 to 180 days of missed payments. A default slashes your score, leads to aggressive collections activity, and can result in legal action. Certain types of defaults, like student loans, can even trigger administrative wage garnishment without court proceedings.

8. Only Making Minimum Payments

Paying only the minimum traps you in a cycle of debt, allowing balances to grow due to accumulating interest. This keeps credit utilization high and suppresses your score. Over time, minimum payments can inflate the debt-to-income ratio.

9. Ignoring Errors On Your Credit Report

Incorrect balances, accounts you never opened, or duplicate records can lurk undetected and quietly destroy your standing. The FTC reports that about 20% of consumers find mistakes in their reports. Left unchallenged, these inaccuracies can cost you important loans.

10. Filing For Bankruptcy Without Exploring Alternatives

Bankruptcy severely punishes your profile, often causing scores to fall by 130–240 points. Chapter 7 bankruptcies linger on reports for as much as 10 years, while Chapter 13 cases stay for seven years. Filing too hastily closes off many future credits, so think before taking that step.

Now that you know what to avoid, here are 10 things you can do instead to increase your credit score.

1. Set Up Automatic Payments

Payment history is the most significant factor in your score. With automatic payments, you’ll never miss due dates, even during busy months. Most banks and lenders offer free autopay services; some even provide small interest rate discounts for enrolling.

2. Pay Down Credit Card Balances Aggressively

Lowering utilization below 30%, and ideally below 10%, can significantly boost your score within a few months. Target the highest-interest balances first to save money while improving the utilization ratio. Even small balance reductions can trigger score increases.

3. Keep Old Credit Cards Open

Even if you no longer use an old card, keeping it open helps maintain a longer average account age and larger total available credit. You could maybe use it occasionally or set up a small recurring charge to avoid closure.

4. Diversify Your Credit Mix

Lenders want to know that you can manage different types of credit responsibly. Having a combination of installment loans (like auto or student loans) and revolving credit (like credit cards) makes up 10% of your score.

5. Dispute Inaccurate Information Promptly

Under the Fair Credit Reporting Act, bureaus must investigate disputes within 30 days. Filing disputes directly with Equifax, Experian, and TransUnion can lead to the quick removal of incorrect late payments or accounts that aren’t yours.

6. Become An Authorized User On A Responsible Person’s Account

When you’re added as an authorized user, the primary account’s positive history is often reflected in your report. This strategy can increase credit scores without requiring a credit check. However, choose someone who consistently pays on time.

7. Open A Secured Credit Card

While this type of card requires a cash deposit, it reports any activity to major credit bureaus. Responsible use can lead to a higher score within six months. Some issuers can upgrade you to an unsecured card after a year of good behavior.

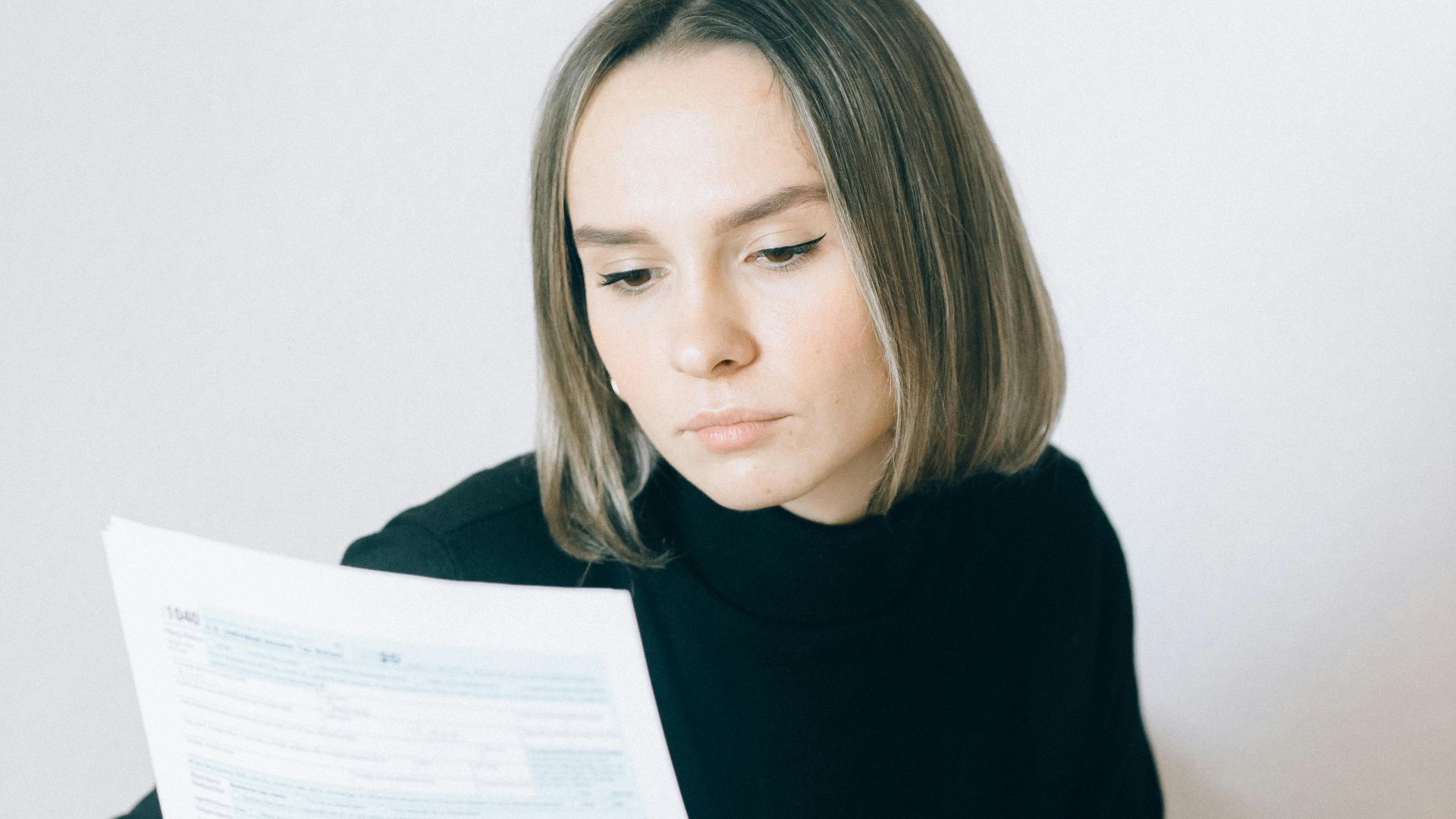

8. Set Credit Alerts And Monitor Your Score

Real-time alerts can help you spot suspicious activity or payment issues on time. Many banks and apps offer free monitoring services tied to your accounts. Regular monitoring also helps you track which actions boost the score fastest.

Tran Mau Tri Tam ✪ on Unsplash

Tran Mau Tri Tam ✪ on Unsplash

9. Negotiate “Pay For Delete” Agreements

Some collection agencies are willing to remove negative accounts from your report in exchange for full or partial payment. Although not all agencies agree to this, getting a written agreement before paying increases the chances.

10. Build Positive Payment History With Credit Builder Loans

Credit builder loans, typically offered by community banks and credit unions, are designed specifically to help improve your score. Payments are reported to the major bureaus, steadily building payment history.