There's More To Money Than Just Spending

It's easy to think money problems come from not earning enough. Sometimes, the real problem lies in how you manage the money you have. Before jumping to quick fixes, it’s important to recognize clear warning signs showing that your money habits might need a serious reset.

1. Avoiding Checking The Bank Balance

Ignoring your bank balance leads to overdrafts and indicates an emotional disconnect from your finances. Behavioral psychology tells us that people avoid uncomfortable situations, often leading to procrastination in managing finances. This can be exacerbated by a phenomenon known as "financial avoidance."

2. Blowing Paycheck On Day One

Spending your paycheck immediately can feel exhilarating, but it's a dangerous habit. Historically, many people lived paycheck to paycheck, particularly during the post-WWII consumer boom when credit cards first became widespread. Mismanaging paydays this way could make it difficult to meet long-term financial goals.

3. Ignoring Credit Score Completely

U.S. legal regulations require that you check your credit report at least once a year for accuracy. Failing to keep tabs on your score can lead to higher borrowing costs or being denied loans outright. It's also vital for major life purchases, such as buying a home, where your credit score plays a significant role.

4. Misuse of Buy Now Pay Later Apps

People tend to overspend when they don't feel the immediate pain of paying for something. This is part of a broader concept known as "hyperbolic discounting." BNPL services can lead to overextension of what you owe, as consumers often forget about the upcoming payments and end up with more debt than they can manage.

Buy Now, Pay Later Apps vs. Credit Cards: The Pros and Cons | WSJ by The Wall Street Journal

Buy Now, Pay Later Apps vs. Credit Cards: The Pros and Cons | WSJ by The Wall Street Journal

5. Living On Credit Cards Monthly

The rise of credit card use in the 1980s, spurred by aggressive marketing, led to a surge in consumer debt. Although CCs offer convenience, they're often accompanied by high interest rates, which can snowball quickly. This practice keeps many trapped in cycles of debt.

6. Borrowing Often From Friends

Borrowing from close relationships can create guilt and shame, leading to strained connections. This can lead to uncomfortable situations, as financial disappointments are one of the leading causes of friendships ending. When friends lend money, it can create a power imbalance in the relationship.

Photo By: Kaboompics.com on Pexels

Photo By: Kaboompics.com on Pexels

7. Having Zero Emergency Savings

The trend of not saving for the future has been prevalent since the 1970s, as consumer spending increased during economic booms. Without an emergency cushion, people tend to rely on loans in times of need, which only compounds financial instability.

8. Using Overdraft Like Free Cash

Overdraft regulations have changed over the years to protect consumers, but it's still one of the easiest traps to fall into. Legal protections around overdrafts were tightened in the U.S. in the early 2000s, yet many still rely on this method to cover short-term gaps.

9. Neglecting Financial Education

Not learning about personal finance puts you at risk for costly mistakes. Knowing the basics—such as how interest rates work, how to manage credit, and how to invest—gives you the tools to make smarter decisions and grow your wealth over time.

10. Confusing Wants With Needs

Consumerism and advertising have led individuals to purchase things they don't need. According to the Consumer Expenditure Surveys by the Bureau of Labor Statistics (BLS), discretionary spending on categories like dining out sometimes comes closer to essential expenses like groceries for some households.

1. Review The Previous Month's Spending

Review your last month’s expenses to identify impulsive purchases tied to emotions. Credit card statements reveal spending habits and expose hidden costs like forgotten subscriptions or unnecessary purchases. This insight helps you spot money leaks and take control of your financial health more effectively.

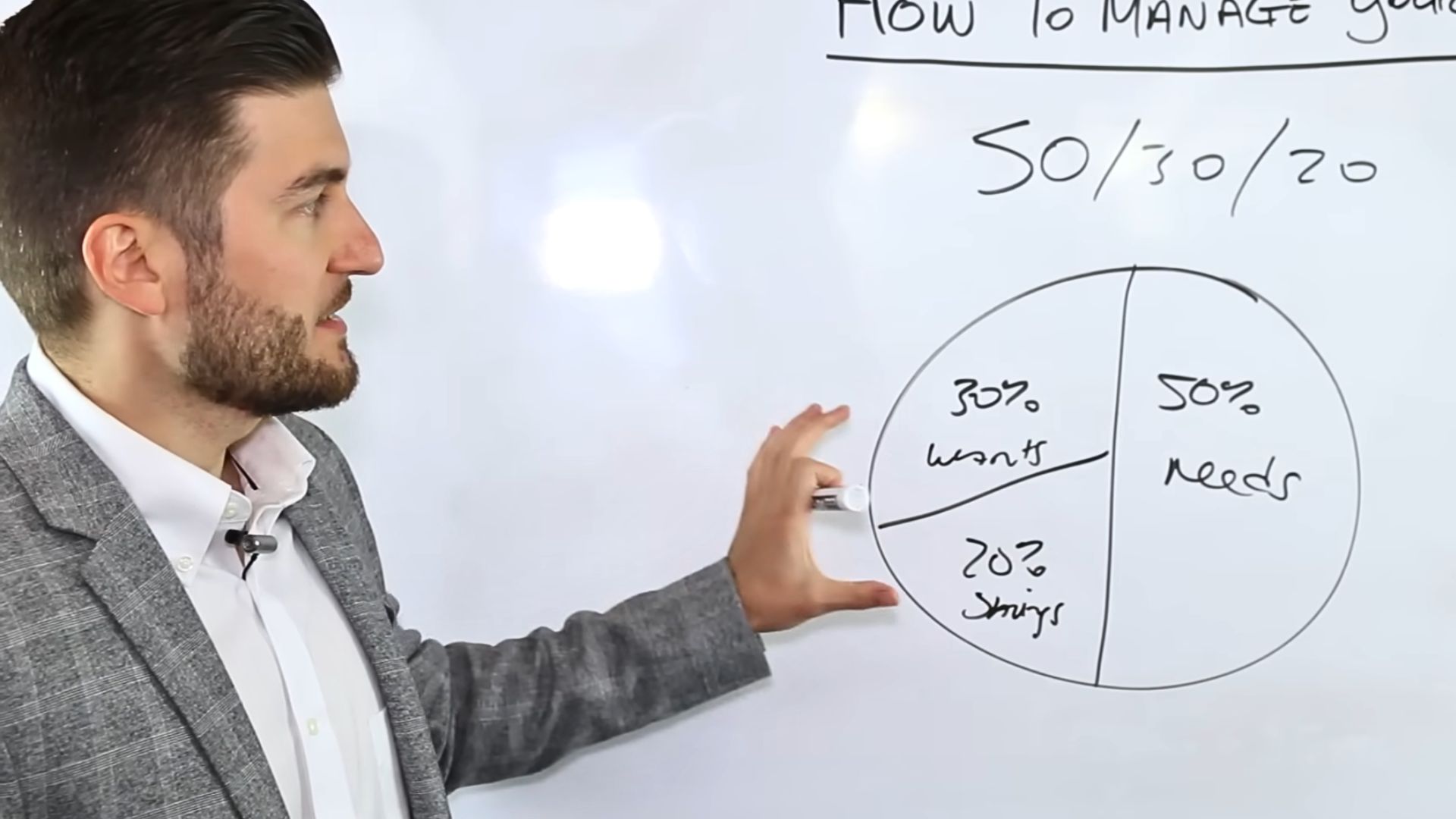

2. Try The 50-30-20 Rule

The framework, popularized by Senator Warren in her 2005 book All Your Worth, separates needs, wants, and savings into manageable slices. While not new, it is a flexible calibration tool that is adaptable to modern budgets with multiple income sources and digital spending channels.

How To Manage Your Money (50/30/20 Rule) by Marko - WhiteBoard Finance

How To Manage Your Money (50/30/20 Rule) by Marko - WhiteBoard Finance

3. Set Up Autopay For Bills

Most banks allow autopay setup for bills like utilities and insurance. Accidentally missing a payment can result in fees and credit score drops. Autopay avoids these risks by making timely payments and improving your credit payment history.

4. Delete Stored Card Details

Retailers often encourage storing your card for "fast checkout," but it's designed to reduce your resistance to spending. The retail industry calls it a frictionless transaction model. Removing stored cards adds a pause for reflection and helps you make smarter financial decisions.

5. Use A Budgeting App

Apps like You Need a Budget or Mint sync with your accounts to check income and categorize expenses. They rely on envelope or zero-based budgeting principles—nothing revolutionary, just digitized. You still make the decisions, but now with clearer visuals and accountability.

6. Track Your Subscriptions

It's easy to forget all those monthly subscriptions, but they add up quickly. Regularly reviewing and canceling unused or unnecessary subscriptions can save hundreds each year. It can provide immediate cash flow relief, allowing for better allocation toward savings or investments.

7. Invest In Long-Term Bonds

Long-term bonds come with penalties if you withdraw money early. U.S. Savings Bonds and Treasury notes that mature in five or more years keep your money locked away, helping prevent impulsive spending. Before investing, consider the impact of interest rates and inflation on your returns.

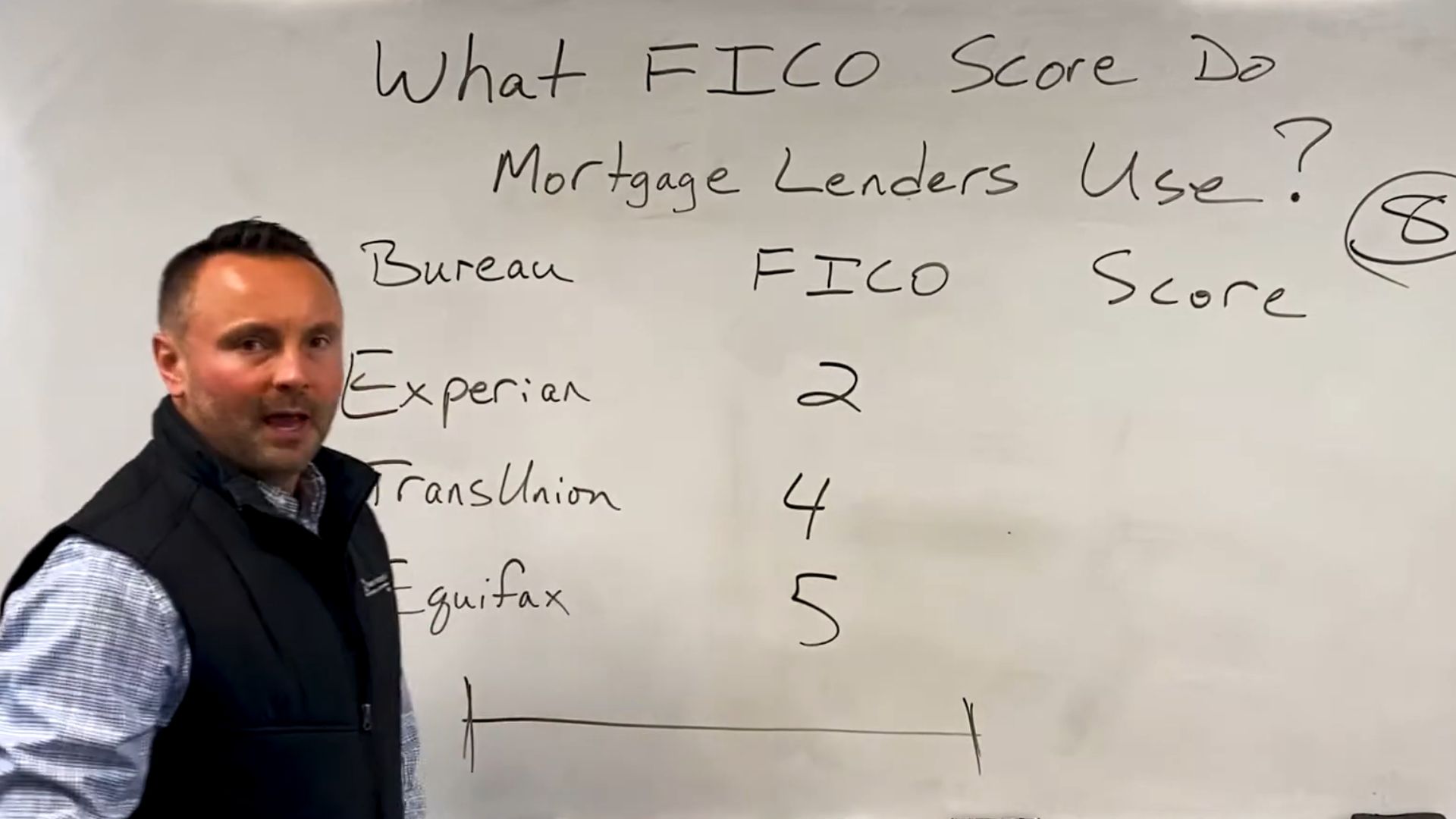

8. Learn How FICO Scoring Works

FICO isn’t mysterious once you know it’s based on five key factors: payment history, amounts owed, credit length, types of credit, and recent activity. This scoring system rewards people who manage credit responsibly over time. Understanding these helps you improve your score.

FICO Score / Algorithm Used By Mortgage Lenders by Premium Mortgage Co

FICO Score / Algorithm Used By Mortgage Lenders by Premium Mortgage Co

9. Use The Cash Envelope Method

Putting physical cash into labeled envelopes feels outdated, but it sharpens emotional spending awareness. You're more cautious handing over a $50 bill than clicking "Buy Now." Popular in the Great Depression and revived during economic crashes, it's a tactile way to give each dollar a job.

Photo By: Kaboompics.com on Pexels

Photo By: Kaboompics.com on Pexels

10. Use Employer Benefits For Savings

Many employers offer benefits like retirement and health savings accounts with tax advantages. These accounts help you save money more efficiently. Besides that, employer matching contributions can boost your retirement savings even more.